Budgeting is one of the most important aspects of managing your finances efficiently. But there are a lot of things that can make this a confusing process, especially if you haven’t done it before. Different types of budgets suit different types of people and you need to figure out what would work best for you. But you don’t have to bust out spreadsheets or hire a financial planner to figure yours out because the 50/30/20 rule is pretty much genius!

One of the easiest ways to make budgeting simple is to use the 50/30/20 rule. This is a budgeting guideline that was popularized by senator Elizabeth Warren through her book “All Your Worth: The Ultimate Lifetime Money Plan”.

As you may have guessed, it breaks down spending and saving into categories to ensure that the money is used in the best way possible. Lots have people have utilized the 50/30/20 tactic competently and you can too!

What is the 50/30/20 rule?

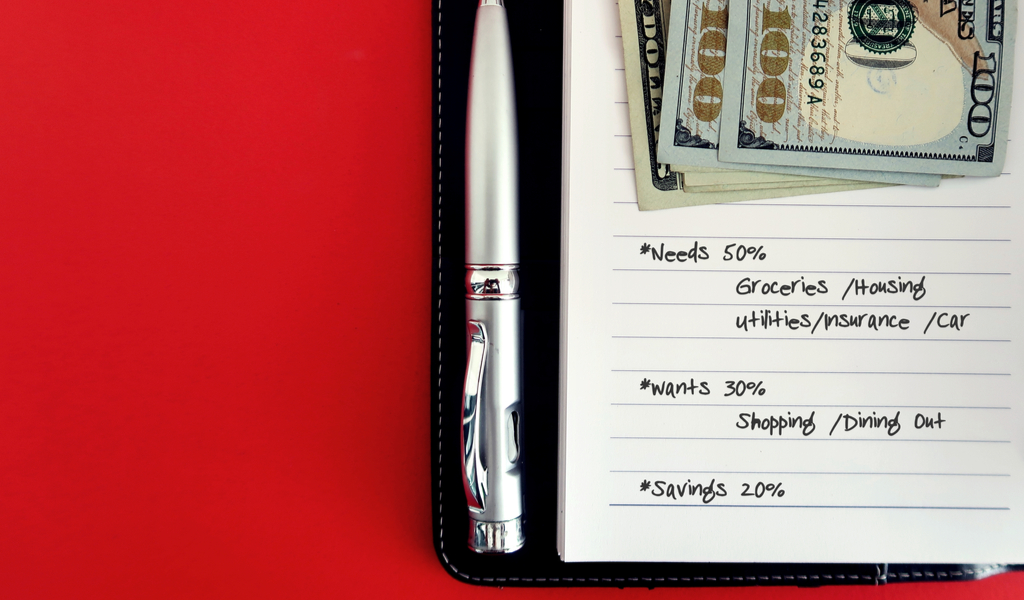

The 50/30/20 rule is pretty simple. It comprises of three different categories: needs, wants, and savings. Let’s break it down:

50% – Needs

The biggest portion of your after-tax income should be allocated to covering your basic needs. These are things that are non-negotiable. You have to pay rent, buy groceries, buy gas for your car, etc. Bills, mortgages, debt payments, transportation, insurance, healthcare, childcare fees, etc. should be covered in this category.

While you must dedicate half your income to this category, it’s important to make sure it doesn’t take any more than that.

30% – Wants

The second-largest portion of your after-tax income is set aside for wants. This category is best classified as “optional spending”. This could be a big purchase that you’ve been wanting to make for a while or things that are non-essential but those that you spend on an average basis.

Everything from concert/movie tickets, dining out, vacations, and shopping for non-essential items (including tech and car upgrades) go into this category. The cup of coffee you get at the local café every morning is counted here too. Even gym memberships of the cable bill would be counted as wants.

20% – Savings

The final category of the 50/30/20 budget plan is savings. 20% of your after-tax income should be put away as savings. You can put it in a savings account, bulk up your emergency fund, or even allocate it towards investments or debt-reduction payments.

How to Get Started with the 50/30/20 budget?

The first step to implementing any kind of budgeting or money management plan is to have a comprehensive idea of how much money you make and how much you spend every month. For most people, their salary makes up the entirety of their monthly income. But if you have any other money coming in from investments, rent, etc. you should count them too. Then you need to determine what all things you spend on every month – everything from your house rent to the bus ride home from work every day.

Now’s the time to break each expense down and file them under the three different categories and adjust accordingly. For instance, if you are having trouble fitting in rent, you should try to cut something from your wants category like canceling that gym membership or cutting down on the number of days you eat outside.

Even after allocating half your income to the needs category, if you find that it’s still not enough, it may be time to make some bigger changes like finding a new apartment or getting a job that pays better. This may seem like a drastic step, but the budget only works if you stay committed to it. It’s best to separate your income into these categories as soon as it hits your bank account or you may never stick to it completely.

Why Should You Choose the 50/30/20 Rule?

Before running for president in 2016, Senator Elizabeth Warren worked as a bankruptcy and personal finance lawyer and then went on to teach law at Harvard University. While there has been debate over whether Ms. Warren was the inventor over the 50/30/20 rule, but there’s no doubt that the former-presidential hopeful was the one who popularized it.

In 2003, she co-wrote a book called The Two-Income Trap along with her daughter Amelia Warren Tyagi, who is a financial consultant herself. The book would become a bestseller and the two financially-savvy ladies would go on to write All Your Worth in 2006.

In it, they introduce and outline the 50/30/20 rule. The book is full of valuable financial lessons such as focusing on the bigger picture instead of obsessing over the small changes.

“Here’s a little secret that the other financial books won’t tell you: Savvy money managers don’t spend a lot of time looking for ways to save a few pennies,” they wrote. “They charge right ahead to the big-ticket items, looking to make high-impact changes in the shortest period of time. They don’t sweat the small stuff. And neither will we.”

The Democratic senator and her daughter say that debt isn’t entirely the fault of the customer as the finance industry and banks actively encourage people to put themselves in such a situation. Ms. Warren warns people not to ignore what she calls “steal-from-tomorrow-debt” such as credit cards of medical bills.

“In today’s world, you can get a mortgage that is too big for you—and the banks will help you do it. You can get a car lease that chews up half your income. You can wind up with a student loan bigger than some home mortgages. And as sure as the sky is blue, you can rack up credit card debt without blinking an eye, even if you don’t have 50 cents to make the payments,” they wrote.

While both ladies are well-versed in the world of finance, they also acknowledge that budgeting isn’t a one-stop solution to fix all your money-related problems. They claim that the 50/30/20 rule is a method for building wealth over a period of time.